Small family businesses are the backbone of our economy, representing the American dream and embodying the essence of what it means to live in a community with one another. There are more than 24.2 million family businesses in the United States, responsible for employing a staggering 62% of the workforce and contributing an impressive 64% of the Gross Domestic Product (GDP). Essentially, the majority of U.S. employees and a large portion of our economic throughput depend on family-run businesses. These entrepreneurial ventures are at the heart of our economy—especially considering the role they serve as living classrooms where the next generation learns family values such as integrity, responsibility, and a strong work ethic. They also model the more practical aspects of business, including developing skills in the financial, marketing, sales, regulatory compliance, and customer service realms. Employees learn firsthand the intricacies of running a company and have an example to follow when considering their dreams of becoming future business owners as well.

Lawmakers have historically recognized the vital role these ventures play in a thriving economy. In response, the Internal Revenue Code (IRC) has been crafted to nurture and support the growth of small family businesses. This has paved the way for a range of tax advantages, specifically catering to the unique needs—and benefits—of family-operated ventures. In fact, the IRS website says, “One of the advantages of operating your own business is hiring family members.”

In this blog post, we will delve into the substantial tax advantages the IRC provides for family businesses, particularly when it comes to parents employing their children.

Our discussion includes:

- Shifting income from parents to children

- Splitting the bill with Uncle Sam

- Roth IRA contributions

- Roth IRA distributions

- Cautions and best practices

Discover how family businesses can effectively leverage tax laws to enhance their financial health while continuing to be stewards of family and community values.

Shifting Income From Parents to Children

One advantage of employing children in the family business is having the ability to shift income from the parents’ higher tax bracket to the lower tax bracket of children. For 2024, the standard deduction for individual filers, which typically includes minors, is $14,600. This means that each child can earn up to $14,600 from employment without incurring federal income taxes. Additionally, since minors are likely to be in a lower tax bracket, they might also benefit from lower state income tax rates, leading to even greater tax savings overall for the entire family.

Consider the Baker family, who owns "Sweet Treats Bakery." The parents are in a high-income tax bracket, let's say 35%. They have three children, aged 13, 15, and 17. If each child is employed at the bakery and earns $14,600 for 2024, the total deduction from the family's taxable income amounts to $43,800 ($14,600 x 3). This can significantly reduce the family's taxable income, potentially saving them $15,330 in taxes (35% of $43,800).

Moreover, the "Kiddie Tax," which typically applies to unearned income like interest and dividends, does not impact earnings from employment. This means that the full benefit of the standard deduction is available for children's earned income without the restrictions that apply to unearned income.

Additionally, employing children in the family business can have implications for the Qualified Business Income (QBI) deduction. Salaries paid to children in the business count as wages for the purpose of calculating the QBI deduction. This is particularly beneficial for parents close to the phaseout range of the QBI deduction, as reducing their taxable income through their children's salaries can increase the QBI deduction they're eligible for and further multiply the tax savings.

Splitting the Bill

Next, let's look at a family-owned clothing store, which the parents use not only to provide for the family but also as a training ground for teaching financial responsibility and independence to their two teenage daughters. Here, we witness a brilliant blend of tax efficiency, business education, and life lessons as these young ladies take on increasing roles of responsibility beyond just being employees. These young ladies are learning what it takes to live independently—yet doing so in a positive atmosphere and under the protective care of their parents.

At the core of this strategy is a simple yet effective idea: shifting financial responsibility from parents to their children. Traditionally, parents bear the costs of their children's needs, from clothes to extracurricular activities. However, in this family, the paradigm shifts. The daughters, aged 15 and 17, are not just helping hands; they are active contributors to the business and, more importantly, to their personal financial journey.

Consider the following monthly expenses that would generally be paid by the parents, but in this case, they are transferring that responsibility to their teenagers.

Monthly Expenses

- Clothing, accessories & shoes: $100

- Personal care & beauty products: $75

- Haircuts & salon services: $25

- Electronics: $75

- Mobile phone, data plans & apps: $100

- Car insurance: $100

- Transportation & gas: $75

- Activities & hobbies: $100

- Personal savings: $75

- College savings: $500

- Spending money: $25

Monthly Total: $1,200Yearly Total: $14,400

From a tax perspective, this approach is not only brilliant but also extremely efficient. These young workers earn up to the standard deduction limit, which is not subject to federal income tax. This means that the money, which would have been taxed at the parent's higher rate, now sits comfortably untaxed at the federal level. The result? A substantial reduction in the family's overall tax liability.

But the benefits of this setup extend far beyond tax savings. By taking ownership of expenses, the daughters are learning the value of money and the nuances of budgeting. They're not just earning—they're learning. This isn't only about getting tax breaks and having fewer expenses for the parents, it's really about empowering these young women with the knowledge and skills they need to be in control of their financial future.

One of my favorite sections of this budget is college savings. Often, parents save a significant amount of their income for their children's college education. Yet, as an advisor, I see children squandering their parents’ money at college, not appreciating the sacrifices their parents made to provide for their future career options and earning potential. Psychologically, however, , when students earn this money themselves, they appreciate it more and are generally more motivated to take advantage of the diverse opportunities their continuing education is affording them.

One thing that is important to point out is that there are particular labor laws established by the Fair Labor Standards Act that limit children's involvement as employees. However, family businesses owned entirely by the parents are largely exempt as long as the work is not dangerous. That said, the employment must be viewed as legitimate by the parents, children, and the Internal Revenue Service (IRS). To establish legitimacy, a simple employment agreement be signed by both parties to document the business arrangement. They ensure the work arrangement is legal, fair, and beneficial for all parties involved. Additionally, consistent record-keeping is essential; an accurate transactional history of payments will be needed to verify the payments.

In the scenario above, employing their teenage daughters in the family business is a multifaceted strategy. It provides income for the children and a smart tax move for them both. Yet more importantly, it’s developing practical life skills in the teens, an essential step towards nurturing responsible, independent young adults.

It may seem risky to put so much faith and trust into the hands of young people. Yet that trust and responsibility are what they so often crave and what they need to mature and develop into successful adults. It is also worth mentioning what an invaluable environment a family-run business is, where they can make mistakes but still have the loving guidance of their parents.

As they interact with the public, handle the cash register, manage inventory, assist vendors, and help with strategic planning, these young ladies are not just helping their family business thrive— they’re setting the stage for their own future filled with infinite opportunities for financial success and independence. This is worth so much more than just sharing income from the family business or splitting the tax bill; it's about instilling real-world responsibilities, values, and lessons that will last a lifetime.

Roth IRA Contributions

Now, let's focus on the opportunity kids have to save for their future, starting as teenagers. One advantage of having kids save their own money for the future is that it shifts the income from the parents’ tax bracket to kids’. And because they’re employed, they are eligible for a Teen Roth IRA.

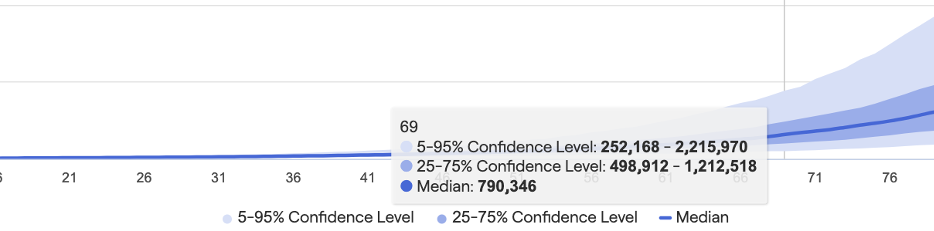

Let's say each child puts in $6,900 ($575 a month) starting when they are ages 13 to 18. Doing nothing else, by the time they are 69 years old, they will have just under $800,000 ($790,364) in tax-free distributions, assuming a 7% growth rate.

Tap into the power of compound interest to do the heavy lifting and create a sizable retirement fund. The tax savings achieved will be exceptional at age 65. They will be able to withdraw all of the $800,000 tax-free, essentially never paying a dime in federal taxes on $800,000.

Roth IRA Distributions

Using the same example of a child who puts $6,900 a year from ages 13 to 18 into a Roth IRA, let’s explore some practical uses for withdrawing some funding from that account, rather than waiting for retirement.

For example:

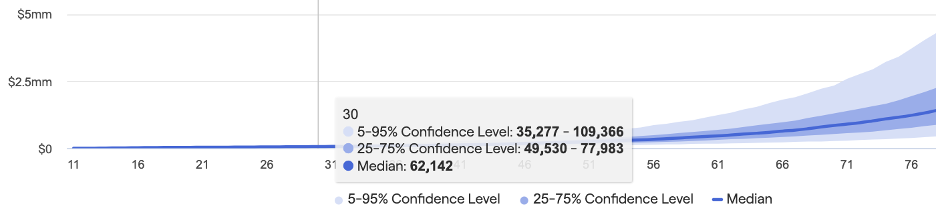

Let's say a child puts in $6,900 starting from the time they are 13 to 18. Doing nothing else and assuming the same 7% interest, by the time they are age 30, they will have $62,142. They could use the first-time home-buyer exclusion to withdraw up to $10,000 for a down payment on their first home.

Additional qualified exclusions include the ability to withdraw $5,000 for every birth or adoption, as well as certain expenses, including qualified higher education costs and unreimbursed medical bills that exceed a certain percentage of your adjusted gross income.

There are so many facets to how significantly working and saving in the early years can set a child up for success throughout their life. It starts by helping develop personal financial management skills needed to be successful. Also, contributing and working for the family business help parents pass on the essential values of strong work ethics, integrity, negotiation skills, making financial decisions, and countless other values that are the true bedrock of a successful life. On top of all that, beginning their savings from a young age will give them the added advantage of the most powerful force on this planet: the power of compounding interest.

Cautions and Best Practices

- Keeping financial and employment records

- Money needs to actually pass from parents to children's accounts. Have a written employment agreement and track hours worked.

- Knowing and adhering to the child labor laws in your state

- While there are no limitations on the age of children working in a family business according to federal regulations, some states have specific laws that you will want to make sure you follow. Also, there may be restrictions on the time of day.

- Dependency Status

- You will still be able to claim your child as a dependent on your taxes as long as you pay more than 50% of their expenses. Considering the cost of housing, food, and things like medical care, parents’ expenses generally exceed 50% of their cost of living. However, it is something to be considered, especially if you live in a very low-cost area or your child is working at another job.

- Reasonable Wage Reasonable Pay

- You will need to pay a reasonable wage for the work they do. While there is plenty of room for interpretation of this, the main idea is you can’t claim you pay your child $100 an hour for taking out the trash or pretend your 5-year-old is keeping the books. Find skills they are legitimately good at—or interested in learning—whether it is fashion design, social media, or even being models for business marketing. Then, you can match that pay with a fair market rate.

- Pay Them Cash

- One legal precedent that has been set with paying children for work is that it needs to be legal tender, i.e., cash, that is paid—not some other form of compensation. In one case, parents paid for pizza instead of the wages and were found ineligible to exclude that amount as income. The money needs to leave your account. You must have documentation showing it left your account and went to theirs. You cannot simply say they received a certain amount without providing proof.

In conclusion, small family businesses serve as both vital economic contributors to our society as well as essential platforms for imparting core values and financial acumen to those coming up the ranks. By thoughtfully involving family members—particularly children—in the business, owners can tap into the tax benefits and income-shifting strategies to enhance their company's financial well-being. More importantly, this practice instills in the next generation valuable lessons about responsibility, a strong work ethic, and the significance of money management. Ultimately, integrating these financial strategies while nurturing family values positions these businesses not only for economic success but also for the cultivation of a legacy enriched with integrity and purpose for future generations.